The Extensions Apple Built and Did Not Ship

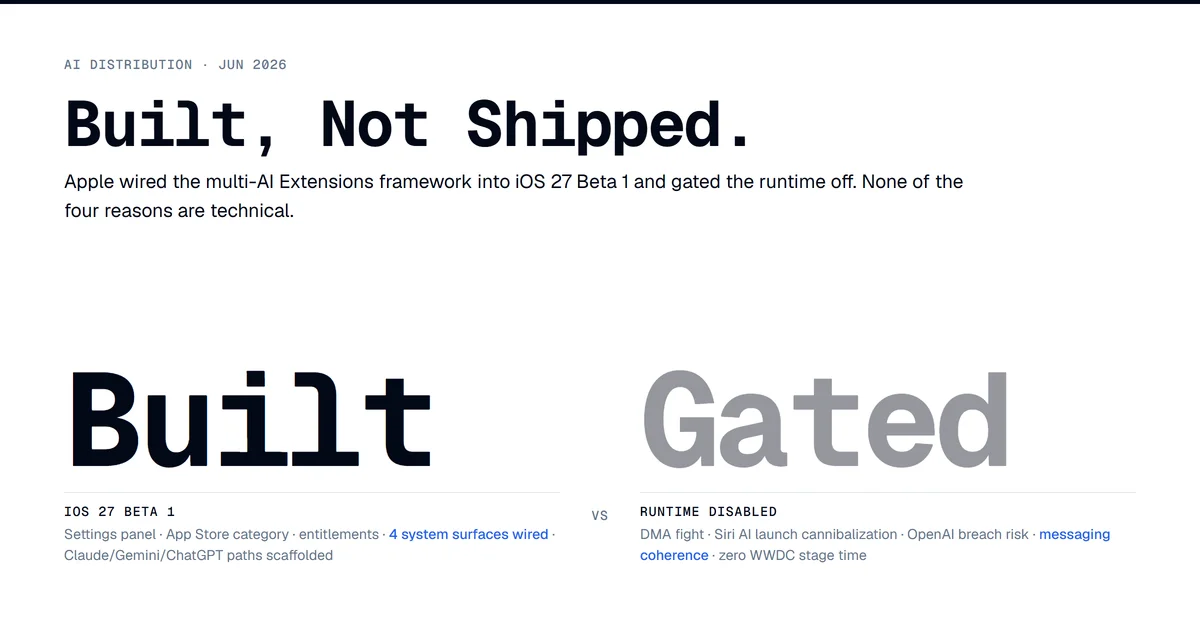

Apple shipped iOS 27 Beta 1 on June 8 with the third-party AI Extensions framework fully built and the runtime gated off. The Settings panel exists. The App Store category exists. The entitlement system exists. The four system surfaces are wired through. The Claude, Gemini, and ChatGPT integration paths are scaffolded. None of it works for an end user, and Apple put none of it on the WWDC stage. TheNextWeb byteiota

That gap — built but not shipped, ready but not announced — is the part of WWDC 2026 worth understanding. The reasons it was deferred are not technical. They are a DMA fight, a Siri AI relaunch Apple needed to land cleanly, a contractual exposure with OpenAI from the iOS 18 era, and a messaging coherence problem. The framework sits in Beta 1 as an option contract on a distribution surface Apple is not yet willing to open.

The Two-Corner Map This Post Updates

Quick recap for new readers. The Unsupervised Agent Tax argued that the consumer AI market is bifurcating by buyer surface, not by model quality. Anthropic took the enterprise floor — ~80% of revenue from API and enterprise commitments, ~1,000 customers at $1M+/year (Sacra), Claude Code at $2.5B+ ARR. Google is trying to own the prosumer subscription before the agent layer commoditizes — Spark on a dedicated GCP VM at $100/month, the $250 tier cut to $200 to bracket ChatGPT Pro. OpenAI keeps consumer scale (800M+ WAUs) but its revenue mix is a different shape than either of the other two.

WWDC 2026 adds a third corner. Apple is not optimizing for model capability or for always-on agent behavior. Apple is positioning iOS as the distribution surface — the place where a consumer's choice among Claude, Gemini, and ChatGPT actually executes, with Apple collecting App Store fees on whatever subscription gets selected. The Extensions framework is how that corner gets built. The fact that the runtime didn't ship in Beta 1 is how Apple is choosing when to open it.

What Apple Actually Announced

Craig Federighi opened the keynote with the first ground-up Siri rebuild in 15 years, rebranded "Siri AI." TechCrunch The new assistant ships as a standalone app on iPhone, iPad, and Mac, with conversation history that syncs across devices, personal context (messages, emails, photos, calendar), on-screen awareness via the Camera app, and multi-step app automation. Federighi described Siri AI as "not a separate chatbot, but rather as an integral but conversational tool that you use in the moment." Variety

The technology underneath is a custom Google Gemini model of approximately 1.2 trillion parameters, built under a roughly $1B/year licensing arrangement Bloomberg has been reporting since January. TheNextWeb Vertu That model is roughly eight times the size of Apple's prior 150B-parameter cloud model and uses Google's mixture-of-experts architecture so only a subset of weights fires per query. The reported topology has Apple licensing the trained weights from Google and running inference on its own Private Cloud Compute servers — Apple-controlled hardware-isolated enclaves — with the contract prohibiting Google from using Apple-routed traffic for training. Introl

One caveat worth flagging. The PCC-only routing is what Apple has communicated and what the analyst writeups have so far accepted. Whether some inference path touches Google Cloud directly — for the largest queries, for fallback, for capability classes Apple's PCC fleet isn't yet sized for — is not independently confirmed. Treat the PCC-only framing as Apple's stated architecture rather than a fully audited fact.

Apple did not say the word "Google" on stage. The Gemini reliance is documented through Bloomberg, Mark Gurman, the Beta 1 framework documentation, and analyst teardowns — not the WWDC keynote, which framed everything as "the next generation of Apple Intelligence." TheNextWeb That omission is not a small detail. It is part of the same discipline that kept Extensions off the stage.

The Extensions Framework That Is Disabled in Beta 1

The Beta 1 developer documentation describes a system where users pick from competing AI providers in Settings → Apple Intelligence & Siri → Extensions and that selection ripples across four system surfaces: the new standalone Siri app, Writing Tools, Image Playground, and the "Search or Ask" natural-language query feature. byteiota AI.cc The framework is built on App Intents — the same containerized, permission-gated extension pattern Apple has used since iOS 8. Discovery happens through a dedicated Extensions category in the App Store.

The Beta 1 code includes all of this. The runtime is disabled on Apple's backend. The first iOS 27 developer beta — shipped June 8, the same afternoon as the keynote — does not let an end user swap Claude in for Siri. TheNextWeb Mark Gurman, whose Bloomberg sourcing on Apple roadmap items has driven most of what the public knows about the Gemini-Siri arc, has reported four reasons it was deferred:

- DMA conflict. Apple is in a regulatory standoff with the EU over the Digital Markets Act (the 2024 law that forces gatekeeper platforms to open core services to third parties) and has argued that opening certain system surfaces creates "unacceptable risks." Announcing a marketplace where users select among Claude, Gemini, and ChatGPT — voluntarily, under Apple's curation — would have made that argument harder to maintain.

- Cannibalizing the Siri AI launch. Per Gurman: "if superior models were available from day one, Apple's own Siri AI would receive less attention." 9to5Mac Gurman's own quality read on Siri AI is that it sits "roughly comparable to where top AI assistants like ChatGPT, Claude, and Gemini were about six months ago." Gurman / Power On The gap is real; the deferral protects it.

- OpenAI litigation risk. The 2024 iOS 18 ChatGPT integration was an exclusive arrangement. OpenAI's lawyers reportedly view the Extensions framework — which demotes ChatGPT from exclusive provider to one option among several — as a potential breach-of-contract event. TheNextWeb

- Messaging coherence. Federighi himself described Siri AI's capabilities as "experimental." Stacking a model-picker alongside an experimental relaunch would have muddied the message that the rebuild works. 9to5Mac

Confidence note on the four-reason list. The DMA and messaging-coherence reads (1 and 4) are also reflected in TheNextWeb's political analysis of the deferral, which lends them a second corroborating angle. The cannibalization and OpenAI-breach reads (2 and 3) trace back to Gurman as the primary source. Gurman's Apple sourcing has driven the public-facing record on the Gemini-Siri arc and has been corroborated repeatedly over the months since January, so the prior on his reporting is strong. But the specific breach-of-contract framing on the OpenAI exclusive should be read as one well-sourced reporter's reading of an active legal posture, not a settled fact. Treat reasons 1 and 4 as well-corroborated, reasons 2 and 3 as Gurman-attributed and reasonable but single-sourced.

Each of those reasons is real. Together they explain why Apple built the framework, scaffolded the App Store category, opened entitlement discussions with all three vendors, shipped the documentation in Beta 1 — and then said nothing on stage.

The $1B Deal Reverses the Existing Apple-Google Money Flow

The Gemini-Siri deal has an underdiscussed property: the money flows the wrong direction relative to the existing Apple-Google search default. For two decades Google has been paying Apple — roughly $20B per year at recent levels — for default search placement on iPhone Safari. Phemex The new arrangement has Apple paying Google about $1B per year for the custom Gemini that powers Siri. Vertu

That reversal matters because it identifies what Apple is buying. Apple is not buying model capability in the abstract. Apple's in-house team has a 3B-parameter on-device model and a previous 150B cloud model, and the "Baltra" silicon roadmap targets H2 2026 production with AI-specific workloads from 2027. byteiota Introl Apple is buying a 24-month bridge. Bloomberg has been describing the deal as "interim until Apple could develop its own foundation models" since January. Search Engine Journal / Bloomberg The Apple-to-Google direction is the price of not being late.

Anthropic's bid was the cheaper-looking alternative that wasn't. Apple evaluated both vendors. Anthropic reportedly asked for more than $1.5B per year with automatic escalators that would have roughly doubled the spend over three years. Search Engine Journal AppleInsider Apple walked. That walk-away matters for the bifurcation thesis. It is a second piece of evidence (after Anthropic's ~80% enterprise revenue mix) that Anthropic is structurally not optimizing for consumer-channel distribution. Anthropic priced like an enterprise vendor offered a consumer-distribution lottery ticket. Apple priced like a buyer who didn't need the ticket badly enough.

The reverse-flow $1B deal does not touch the existing $20B/year search payment. That deal continues to flow Google-to-Apple. Net cash flow between the two companies still favors Apple. What changed is that Apple has now demonstrated willingness to pay Google for a piece of compute capability — which gives Google a small piece of leverage in the next search-default renegotiation. One analyst reads it as "Apple gains negotiating leverage on future search payments by offering Gemini distribution." Phemex That reading may be optimistic. The direction-of-leverage question is genuinely uncertain and depends on how the Justice Department's pending search-monopoly remedies land. Both directions are defensible from the current evidence.

Re-pricing the Consumer AI Bifurcation

The original two-corner thesis was: Anthropic took the enterprise floor; Google is trying to own the prosumer subscription before the agent layer commoditizes. The thesis stood up because each vendor was running a different play on a different surface — Anthropic compounding enterprise procurement, Google productizing the $100 24/7 VM through Spark.

Apple's move adds a third corner that is structurally different from either. Apple is not optimizing for model capability or for an always-on agent. Apple is positioning the iPhone as the distribution surface itself — the place where a consumer's choice among Claude, Gemini, and ChatGPT actually executes. The Extensions framework, if it ships, makes Siri a routing layer rather than a model. The user picks the provider; the OS routes the request; the provider does the work; the provider gets paid by the user; Apple takes its App Store cut on the subscription.

The structural reading: Apple has decoupled three layers that used to be fused in the consumer AI market.

| Layer | Owner under old model | Owner under iPhone Extensions model |

|---|---|---|

| Model capability | ChatGPT, Claude, Gemini each owned their stack end-to-end | Same — vendors own the model |

| Subscription billing | Each vendor sold direct via web | App Store (Apple takes 15-30%) |

| OS-level distribution | Each vendor competed for app-icon real estate | Apple owns the routing surface |

The third row is the one that did not exist before. Routing has always been the user opening a specific app. Apple is proposing that routing moves into the OS, with vendor choice as a Settings menu, and the consequence is that vendor switching cost collapses to one tap. That hits the bifurcation thesis from the side, not head-on.

- For Anthropic: the enterprise floor stays untouched, and the consumer-channel question they answered by NOT bidding hard for Siri stays answered. But Extensions, if shipped, gives Anthropic a free distribution surface on the iPhone install base — at no cost beyond an entitlement and an App Intents implementation. That is a strict upside relative to status quo. Anthropic owns no consumer surface today; Extensions creates one without Anthropic having to fight for it.

- For Google: the $1B Apple deal is the cost of being the default. Extensions, if shipped, dilutes that defaultness — but Google still keeps the underlying Gemini bill, and Google's own prosumer subscription (Spark at $100/mo) sits one layer up from the iPhone surface and is unaffected by who Siri routes to.

- For OpenAI: the current iOS 18 exclusive deal is the asset Extensions would erode. The reported breach-of-contract posture suggests OpenAI knows this. ChatGPT today has the largest installed consumer iOS footprint in AI — already integrated, already exclusive. Extensions converts that into one option among three.

- For Apple: the prize is becoming the toll-collector on a distribution surface vendors cannot reach without Apple's permission. The historical analogy is the App Store itself. Apple did not build the apps people wanted to use; Apple built the distribution layer underneath them and collected on transactions.

That last bullet is where the Extensions framework becomes the most strategically valuable piece of iOS 27. The surface is too valuable to launch in the middle of a regulatory fight, an OpenAI legal exposure, and a Siri AI relaunch. So Apple shipped the code, deferred the runtime, and waited.

One genuine unknown worth naming. Apple has not disclosed the revenue model for Extensions itself. The default assumption — App Store cut on the subscription a user buys from a third-party AI provider — is the natural extrapolation from existing App Store economics, but Apple has not confirmed it as the Extensions model. A revenue-share arrangement with the provider, a flat-fee entitlement, or an enterprise-Volume-Purchase-style structure are all possible. The 15-30% framing in the table above is the most likely shape based on existing patterns, not a published number.

What This Means for the Bifurcation Thesis

The two-corner thesis does not collapse. It extends. Anthropic still has the enterprise floor — nothing at WWDC 2026 changes the 80% enterprise revenue mix or the absence of a consumer agent. Google still has the prosumer subscription play — Spark at $100/mo, 24/7 VM, doesn't compete with iPhone Extensions because it operates one layer up. What Apple added is the third corner: the distribution toll. The consumer pays the vendor; the vendor pays Apple; Apple owns the routing surface.

The consumer-AI map after iOS 27 ships (assuming Extensions runtime ships within the 27.x cycle):

| Layer | Anthropic | OpenAI | Apple | |

|---|---|---|---|---|

| Enterprise procurement | dominant | growing | present | n/a |

| Prosumer subscription | minor (Claude Max) | dominant (Spark) | dominant (ChatGPT Pro) | n/a |

| Consumer chat | catching up | growing | dominant | n/a |

| iPhone distribution | new option | partner + option | erstwhile exclusive | toll-collector |

Apple's role is structurally different from the others. It does not have a model to monetize. It has roughly 1.5 billion devices byteiota where the AI gets consumed and (presumed) App Store economics on whatever subscription the consumer picks. The vendor that captures the most iPhone Extensions selections will earn the most consumer subscription revenue, and Apple will take its cut across all of them.

What Builders Should Watch

Three operational reads.

For consumer AI vendors: the Extensions runtime ship date is the leading indicator. If Apple ships it in iOS 27.0 in September, the consumer iPhone surface opens immediately and the competition for Settings-menu placement becomes the new growth lever. If Apple ships it in a 27.x point release later, vendors have more time to build polished iPhone apps that the Extensions choice would direct traffic to. If Apple does not ship it at all in the iOS 27 cycle — possible given the four reasons above — the existing iOS 18 ChatGPT exclusive deal hardens for at least another year.

For app developers more broadly: the App Intents requirement is the actual story. Apple's framework documentation is explicit that Extensions and Siri AI both route through App Intents. byteiota App Intents have been a public API since iOS 16, so this is not net-new work for actively maintained apps. What changes is the cost of skipping it: any app that does not expose its core actions as App Intents becomes invisible to Siri AI, regardless of which AI provider the user picks. The developer-discourse thread from @thepanshi_ identifies seven app categories most exposed to this routing shift: voice/dictation, automation, launchers, single-purpose utilities, smart-home, parental controls, and a handful of utility wrappers. thepanshi_ Call it the App Tracking Transparency moment, round two — same structural pattern, different lever.

For prosumer subscribers doing the spend audit: the value proposition of a $20/mo Claude Pro or Gemini AI Pro subscription on iPhone changes the moment Extensions ships. Today those subscriptions buy access to that vendor's standalone app. Post-Extensions, the same subscription buys system-wide access — Writing Tools, Image Playground, Siri requests — without leaving the OS. That is a meaningfully different product. The $100 Gemini AI Ultra tier (Spark + VM) sits outside this calculus; Spark is a different category than Extensions provider selection.

What Apple Decided Not to Decide

The piece of WWDC 2026 worth holding onto is what Apple deferred. The Gemini-Siri integration shipped. The Extensions framework deferred. Apple's own foundation-model roadmap (Baltra silicon, 2027) is on a multi-year clock. The OpenAI exclusive deal is in legal limbo. The DMA fight is unresolved. Apple bought a 24-month bridge with Gemini and gave itself flexibility to ship Extensions whenever those four constraints relax.

Apple is not trying to win the model layer. That is settled in Google's favor for now and Apple's in-house team will pick up the contest in 2027. What Apple is trying to win is the distribution layer. The Extensions framework is the option contract on that win. It gets exercised when the regulatory and contractual situation lets it. Until then, it sits in Beta 1, fully built, gated off.

A natural question is whether a competitive Baltra-era Apple foundation model in 2027 kills Extensions before it ships. Probably not. The toll-collector position does not require Apple to lose the model layer; it requires Apple to own the routing surface. Even if Apple's own model becomes the default Siri AI provider in 2027, Extensions still gives the OS a way to monetize the users who prefer Claude or Gemini. The framework hedges Apple against both outcomes — a strong in-house model and a weak one. The deferral is paced by the legal calendar; the model roadmap is a separate clock.

Anthropic took the enterprise floor. Google bought the model layer and is trying to own the prosumer subscription. Apple just built the toll booth. Whether the booth opens this fall, next spring, or never depends on a set of legal and regulatory variables that have nothing to do with whether the technology works.