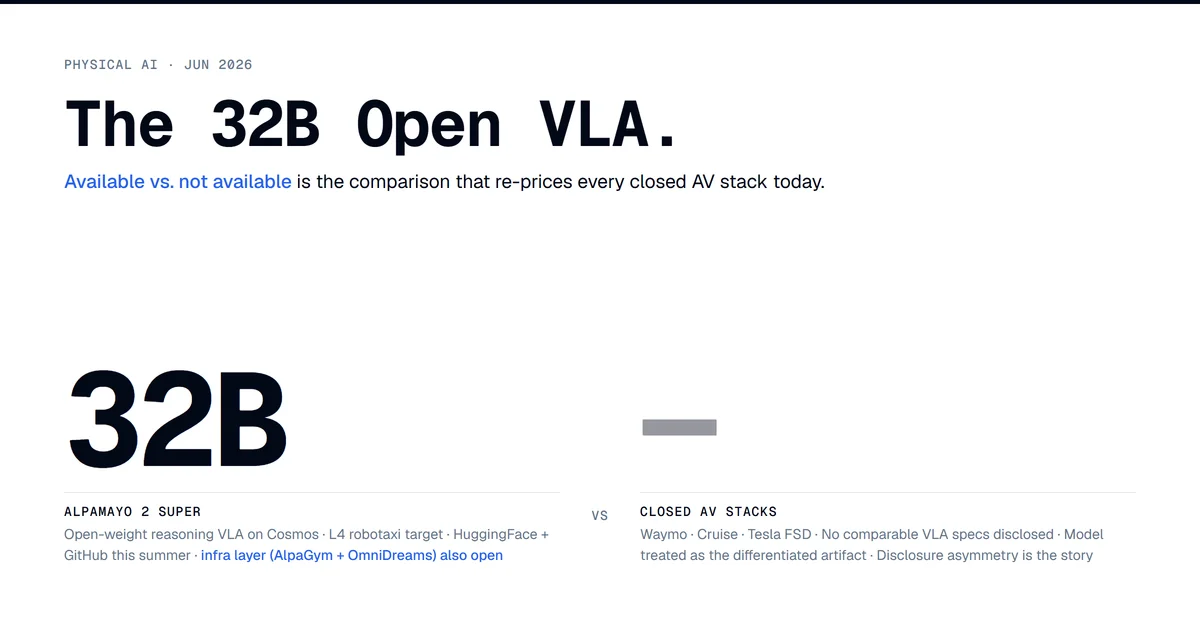

The 32B Open VLA Re-Prices Every Closed AV Stack

NVIDIA shipped Cosmos 3 on HuggingFace today and put a 32-billion-parameter reasoning Vision-Language-Action model on a summer release calendar, with Level 4 robotaxi developers named as the target customer in the press release. Alpamayo 2 Super is the VLA. Cosmos 3 Super and Nano are the world-model foundation it sits on. The chip vendor that sells GPUs to every closed AV lab on the planet just open-weighted the model layer above its own silicon. None of the closed labs (Waymo, Cruise, Tesla FSD) disclose comparable VLA specs in public, so there is no head-to-head to run. The comparison being made today is available vs. not available, and that is the comparison that re-prices the stack.

That sentence is the whole story. The rest is technical context for readers who haven't been watching the physical-AI release calendar, the structural reason this matters more than a benchmark win, and the four things I would be tracking if I were running procurement at a Tier 2 AV program right now.

What NVIDIA Actually Shipped Today

At GTC Taipei (co-running with Computex), NVIDIA dropped four artifacts in one release window.

Cosmos 3 is an omnimodel for physical AI in two open-weight variants today: a 64B Super (32B reasoner tower plus 32B generator tower) and a 16B Nano (8B plus 8B). An Edge variant is announced but not released. The architecture is a Mixture-of-Transformers, with an autoregressive vision-language reasoner paired with a diffusion world-generator, sharing a token interface. NVFP4 quantization and Efficient Video Sampling ship in the inference path. Super targets Hopper and Blackwell datacenter GPUs; Nano runs on an RTX PRO 6000 workstation. See the HuggingFace Cosmos 3 blog and the NVIDIA developer blog for the architecture write-up.

Alpamayo 2 Super is a 32B reasoning VLA built on Cosmos, announced today, with weights and inference code arriving on HuggingFace and GitHub this summer. Three times the parameter count of Alpamayo 1 / 1.5 Nano. 360-degree perception (the prior generation was forward-only), 3D scene understanding, meta-actions for yield, stop, and lane change, and an interpretability surface for safety validation. The NVIDIA newsroom names L4 robotaxi developers as the target customer in the headline.

AlpaGym is an open-source high-throughput closed-loop reinforcement-learning framework for AV stacks. The pitch is training against compounding errors and edge cases rather than against static datasets, which is what closed-loop simulation buys you over open-loop replay.

OmniDreams is a generative world model under the NVIDIA Agent Toolkit umbrella, photorealistic, designed for long-tail driving scenario synthesis at scale.

Add Nemotron 3 Ultra (550B sparse Mixture-of-Experts, 55B active, Artificial Analysis intelligence index of 48, the top US open-weights LLM at release per Artificial Analysis) and you have the full posture. The chip vendor is shipping open-weight artifacts up and down the stack. The model card SPDX should be consulted on the Cosmos3-Super HuggingFace page before any open-source claim, because the licence is described in the blog post as NVIDIA's permissive open model licence with commercial use allowed, but the exact name was not in the press materials I read. The mechanically true wording today is open-weight, and that is what I am using.

What a VLA Actually Is, and Why 32B Open Matters

For readers new to the embodied-agent vocabulary: a Vision-Language-Action model is the single network that takes camera (and sometimes lidar / radar) input, fuses it with a text description of the task or scene, and emits the action. For a robotaxi that means steering, throttle, brake, and the discrete meta-actions like yielding to a crossing pedestrian or aborting a lane change. The older AV stack design splits perception, prediction, planning, and control into separate modules with hand-engineered interfaces between them. The VLA design collapses the back half of that pipeline (prediction, planning, control reasoning) into one learned model that can be trained end-to-end and validated as a single artifact.

The reason 32B open weights re-prices the closed stack is not that 32B is frontier-scale by LLM standards. It isn't. The reason is that the closed AV labs treat the VLA as their differentiated artifact. The data flywheel is real but commoditizing fast (every L4 program is logging real-world miles, and OmniDreams now synthesizes the long tail). The compute is rented from NVIDIA either way. The simulator stack is now also open via AlpaGym. The model is the differentiator. If a 32B open VLA from the chip vendor is downloadable and runnable, the differentiator collapses to three things: the data you can collect that the open training set can't, the safety case you can write, and the deployment footprint you can operate. Those are real things to win on. They are also not what most closed AV pitch decks emphasize.

Two procurement-relevant facts about the Alpamayo 2 release that nobody is reading carefully enough yet.

- The target customer is named in the press release. Level 4 robotaxi developers is in the headline of the NVIDIA newsroom post. That is a specific procurement category, not a generic robotics positioning. NVIDIA is telling the L4 buyer the model is for them.

- The infrastructure layer is also open. AlpaGym and OmniDreams are the training and validation surface, not just the inference artifact. A closed lab has to argue that their internal sim stack plus their internal RL framework plus their internal VLA is collectively worth more than the open stack plus their internal data. Each component the open release covers shifts that argument.

What the release doesn't disclose, and what I am not going to invent: benchmark numbers. NVIDIA claims leadership on VANTAGE-Bench, PAI-Bench, R-Bench Physics-IQ, and RoboLab leaderboards (in the open-source category for the relevant scales) without publishing scores in the launch materials. The dev blog references those benchmarks; the scores are presumably in the model card or a paper that hasn't dropped. The honest claim today is that the artifact is available with a specified architecture and parameter count, target customer named. The performance claim is the next post, after the model card is out and somebody outside NVIDIA has run it.

The LLM Parallel Without the Headline Compression

The temptation, when a major lab open-weights a frontier-tier artifact, is to reach for the DeepSeek analogy. I am going to use the parallel for structure and then walk away from the framing, because the framing flattens what is actually different here.

The LLM parity moment hit on a known timeline: DeepSeek V3 in December 2024, V4 in April 2026. V4-Pro is MIT-licensed, 1.6 trillion total parameters, 49 billion active, hits 80.6% on SWE-bench Verified, and ships from a Chinese chip-adjacent lab that openly notes its compute base is constrained until Huawei Ascend 950 scales. The release shape was a scrappy challenger lab, chip supply asymmetry, fully open weights, frontier-tier benchmarks, repriced cost curve. Closed US labs spent the next eighteen months explaining to procurement why their gated APIs are still worth the premium over a 1.6T artifact you can run yourself.

Cosmos 3 plus Alpamayo 2 Super is the structurally same-shape release for embodied agents. Open weights, top-of-stack scale for the category, the infrastructure layer also open, repricing the closed AV stack. The asymmetry is the opposite, though. NVIDIA is not a scrappy challenger. NVIDIA is upstream of every closed AV lab and every closed frontier LLM lab. The chip vendor open-sourcing the model that runs on the chip vendor's GPUs is a different commercial signal than a challenger lab open-sourcing to break a monopoly. It is closer to a platform deepening. NVIDIA is making the upper layers cheaper to commodify everything except the GPU, which is the layer NVIDIA sells.

That is the reason I am refusing the familiar one-line framing for this release. Same artifact shape, opposite incentive geometry. The familiar template would compress a meaningfully different commercial situation into a recycled headline. The familiar template would also be the easiest tweet to write today, which is usually the signal that it is wrong.

The procurement-inversion essay from May 7 had the same structural payoff and is the closest tangential prior in this catalog. There I argued that DeepSeek V4 plus the Mythos gating context meant US-headquartered enterprises were genuinely asking whether self-hosting Beijing-trained model weights was the path of least compliance friction. The Cosmos 3 release reads the same way for a different category. The question of whether an open-weight 32B VLA from NVIDIA is a credible substitute for a closed proprietary VLA from a Tier 1 AV lab is now a real procurement question, not a thought experiment.

The Three-Tier Frame Extends Cleanly

Cosmos 3 ships as three explicit deployment tiers, and the alignment with the inference-economics framing DDT has been building is the cleanest part of the release.

| Tier | Variant | Target hardware | Status today |

|---|---|---|---|

| Datacenter | Cosmos 3 Super (64B total: 32B + 32B) | Hopper / Blackwell | Released |

| Workstation | Cosmos 3 Nano (16B total: 8B + 8B) | RTX PRO 6000 | Released |

| Edge | Cosmos 3 Edge | Real-time, hardware TBD | Announced, not released |

This is the same three-tier decomposition the procurement-inversion essay argued was the hidden architectural decision for LLMs. NVIDIA is now making the decomposition explicit at release time for physical AI, with the same model family scaled across tiers. The Super-Nano-Edge naming is not marketing dressing. It is an admission that the cloud, workstation, and vehicle deployment surfaces have different inference-cost profiles, and the model family has to be designed for them in advance.

For an L4 robotaxi program, the realistic deployment shape probably looks like this:

- Datacenter (Super) runs training, simulation-at-scale via AlpaGym plus OmniDreams, fleet-wide replay for auto-labeling and edge-case mining.

- Workstation (Nano) runs engineer development loops, shadow-mode validation, and on-call investigation rigs.

- Vehicle (Edge) runs real-time inference inside the car. Hardware target is presumably Drive Thor or a successor, but the Edge variant hasn't shipped and the press release doesn't commit to specifics.

If you have read the procurement-inversion essay, this is the embodied-agent extension of the same argument. Inference-tier choice is the architectural decision. The model family has to acknowledge the deployment surface. The open-weight artifact at the right tier is what makes the deployment economics close.

Where I Would Be Cautious

A few things I am explicitly not claiming, because the press materials don't support them and I would rather be slow than wrong.

- No Alpamayo-beats-Waymo claim. Closed AV labs don't publish comparable VLA specs. Any comparison would be Alpamayo disclosing what closed labs don't, not Alpamayo winning on a specific axis. The disclosure asymmetry is the actual story; the performance comparison is a vacuum.

- No benchmark numbers from NVIDIA's claimed leaderboard wins. The dev blog references VANTAGE-Bench, PAI-Bench, R-Bench, and RoboLab without scores. Until the model card or the technical report drops with specific numbers, the responsible read is claimed leadership, scores pending.

- No assumed licence terms for Alpamayo 2 Super. The press materials do not specify the licence. Cosmos 3 is NVIDIA's permissive open model licence with commercial use allowed per the HuggingFace blog. Alpamayo could be the same, or could be more restrictive (NVIDIA has historically attached usage carve-outs to AV-related artifacts). Wait for the model card.

- No assumed partner or pilot list. Prior Alpamayo (1 / 1.5) cycles were covered as ecosystem partnerships with Mercedes-Benz, Lucid, JLR, Volvo, and Continental. Today's press release names none of them specifically for Alpamayo 2 Super. Whether prior partnerships carry forward to the 2 Super release is unconfirmed.

- The physical-AI-parity framing is overheating. Open weights with named target customers is a real commercial inflection. It is not the same as a claim that the closed AV stacks are obsolete this morning. Operating an L4 robotaxi service is not a model-weights problem. Cosmos 3 changes the model-layer economics; the deployment economics (vehicles, fleets, ops, insurance, regulators) are unchanged.

What I Would Be Tracking If I Were on the Buy Side

Four signals that will tell us whether this release re-prices the closed AV stack in practice, or just on Twitter.

- Tier 2 AV programs naming Alpamayo 2 Super in pilot announcements within 90 days of the summer release. Lucid, JLR, Volvo, Continental, and the second-tier Chinese robotaxi operators are the realistic adopters. If three or more of them name Alpamayo specifically (not Cosmos generically) by end of Q3 2026, the model layer is moving.

- A closed AV lab publishing comparable VLA specs in response. Waymo, Cruise, and Tesla FSD have been comfortable disclosing nothing about their internal model architectures. If any of them publishes a parameter count, an architecture description, or a benchmark number in the next 90 days, the disclosure asymmetry is breaking. The opposite read, silence, means the closed labs are betting that data plus operational footprint is enough differentiation on its own.

- The Cosmos 3 model card SPDX. Verify the licence is what the HuggingFace blog implies. If it is the NVIDIA Open Model Licence used for Nemotron and earlier Cosmos, the commercial terms are familiar. If it is a new licence with AV-specific carve-outs, that is news.

- Whether Edge ships before end of summer. The Edge variant is the one that determines whether Cosmos 3 is a real three-tier release or a two-tier release with a roadmap. The robotaxi compute target is in the vehicle, not in the cloud. Without Edge, Alpamayo 2 Super on-vehicle inference is a story about Drive Thor optimization, not about Cosmos.

Each of these is a falsifiable signal on a 90-day clock. If three out of four resolve as predicted, the model-layer story is real. If two or fewer, the closed AV stacks survive the release with their valuations intact.

The Stake DDT Is Planting

This is the first post on this site about physical AI specifically because the structural inflection that hit LLMs in late 2024 just arrived for embodied agents, and the model layer is no longer the differentiator for closed AV stacks.

The bet I am making by writing this is that the people reading DDT for the LLM-procurement framing are going to be asked the embodied-agent version of the same question by a board, by a CIO, by a fleet operator, by an insurance underwriter, within the next eighteen months. The honest analyst answer is that the model layer is open at the relevant scale, the infrastructure layer is open, the chip vendor is the one open-sourcing it, and the closed AV labs have not yet published anything that explains why their model is still worth the closed premium. That answer is harder to defend the longer the closed labs stay quiet.

If you want the LLM-side parallel, the procurement-inversion essay is the prerequisite read for what happens to enterprise procurement when the open-weight artifact reaches frontier-tier. The next post in this thread is the model-card read once NVIDIA publishes the SPDX and the benchmark scores.